Why tax is the first thing to plan

When you sell your business, the headline price isn't what you keep. Between the amount agreed with the buyer and what actually lands in your bank account, tax is usually the single largest deduction — often hundreds of thousands, sometimes millions of dollars.

And yet most owners of Quebec SMEs only think about tax at closing, when it's too late to optimize anything.

That's an expensive mistake. Tax planning isn't a last-minute detail — it's the first variable to consider, ideally 12 to 24 months before the sale.

Why that early? Because the decisions with the biggest impact on your net proceeds — the sale structure, eligibility for the Lifetime Capital Gains Exemption, the need for a corporate reorganization — all take time to put in place properly.

Here's what's really at stake: two comparable businesses sold at the same price can leave very different net amounts with their owners. The difference usually comes from the structure chosen and the preparation done upstream.

Share sale or asset sale, real eligibility for the Lifetime Capital Gains Exemption, allocation of the purchase price across asset categories — each of these decisions moves the needle.

The tax specialist plays a central role in this equation. They don't replace your business broker or your lawyer — they complement them. The broker runs the sale process, the lawyer protects your interests in the agreement, and the tax specialist makes sure the structure maximizes what you keep after tax.

These three professionals have to work together, and the earlier the tax specialist is involved, the more room they have to optimize. Our guide walks through the team of professionals you need to sell a business in Quebec and the role each one plays in the transaction.

This guide covers the big tax questions raised by the sale of a Quebec SME. Its goal isn't to replace your tax specialist — that would be irresponsible. It's to help you grasp the issues, ask the right questions, and make informed decisions.

The capital gain and the Lifetime Capital Gains Exemption

Two tax concepts dominate every conversation about selling an SME in Quebec. Your accountant mentions them, your banker asks about them, and your broker structures the transaction around them.

Understanding them, even in broad strokes, lets you ask your tax specialist the right questions and take an active part in the decisions.

THE CAPITAL GAIN

When you sell an asset for more than its tax cost, the difference is a capital gain. In a business transaction, the exact calculation depends on the sale price, the adjusted cost base (ACB), certain expenses, and the structure chosen.

A capital gain receives more favorable tax treatment than ordinary income: only a portion of the gain is included in your taxable income, under the rules in force on the date of the sale. (Source: Canada Revenue Agency, 2025.)

It's a meaningful advantage. By comparison, a dollar of employment income is taxed in full, while a dollar of capital gain is only taxed in part. For an owner selling after years of work, that difference can mean tens, even hundreds of thousands of dollars kept in their pocket.

THE LIFETIME CAPITAL GAINS EXEMPTION ON QSBC SHARES

This is the most powerful tax benefit available to a Canadian SME seller. The Lifetime Capital Gains Exemption (LCGE) allows, under specific conditions, a significant portion of the gain realized on the sale of qualified small business corporation (QSBC) shares to be sheltered from tax.

The applicable cap depends on the year of disposition. For reference, the Canada Revenue Agency indicates $1.25 million for 2025 for eligible dispositions (source: CRA, 2025 taxation year). This amount can be adjusted or indexed later, so always validate the actual year of your transaction.

Qualifying for it is more than a label: being a CCPC isn't enough on its own. In practice, your tax specialist checks several tests, including:

- The company must be a CCPC and the shares sold must be qualified small business corporation shares — not simply shares of a company that looks active.

- At the time of the sale, the company must generally meet the "all or substantially all" test: the assets used principally in an active business carried on in Canada must represent about 90% or more of the fair market value of total assets, based on the tax specialist's analysis.

- Throughout the 24 months before the sale, more than 50% of the fair market value of the assets must generally have been used in the active business, and the shares must have been held by you or by a person related to you.

Illustrative example

Picture an owner who sells the shares of their manufacturing SME for $3 million. Their adjusted cost base is minimal, so almost all of the proceeds correspond to an economic capital gain. If the shares are qualified and the Lifetime Capital Gains Exemption applies, the tax saving can be on the order of several hundred thousand dollars, depending on the year of sale, the province, and the seller's personal situation.

Note: the figures above are illustrative. The exact exemption amount, inclusion rate, and effective tax depend on the year of the transaction, the province, and your situation. Always check these parameters with your tax specialist.

What can cost you eligibility: too many passive assets inside the company, a building not used in the active business, accumulated investments, shareholder loans, or a reorganization done too late. That's why we talk about corporate purification well before the sale — a technical exercise that takes time, documentation, and a tax specialist involved early.

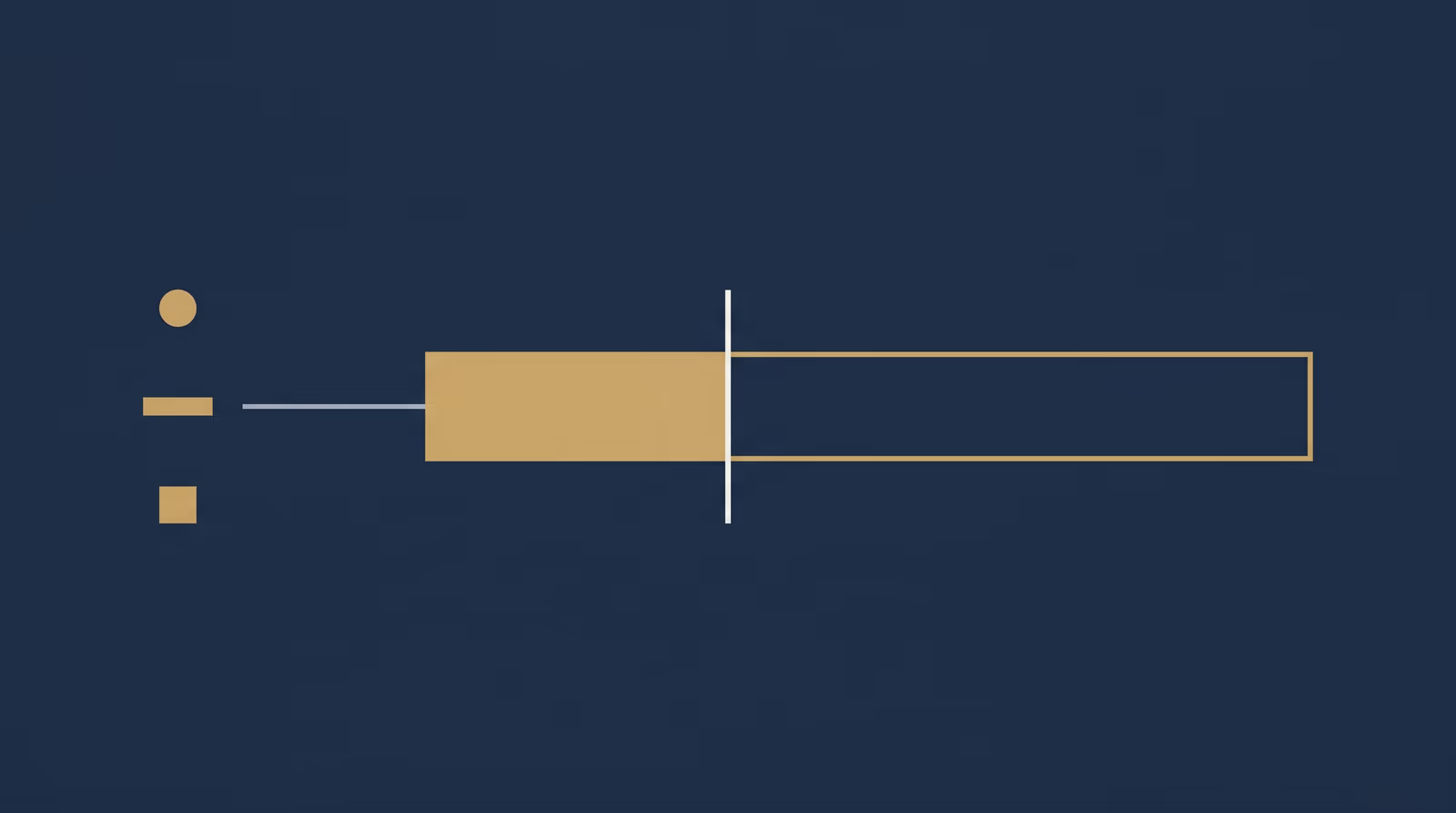

What's left after the sale: the real math

Here's the question every owner asks — and too few actually run the numbers on before committing: how much do I really keep? The sale price is an impressive figure on paper. What matters is the net amount left once every deduction is accounted for.

Between the headline price and your bank account, several items pull the number down:

- Tax on the capital gain — The taxable portion of the gain, after the exemption applies where available, is added to your income under the rules in force for the year of the sale. This is usually the largest single item.

- Professional fees — Business broker, lawyer, accountant, tax specialist. These fees are legitimate and necessary, but they add up. Depending on the size and complexity of the transaction, this line should be modeled ahead of time rather than assumed after the fact.

- Debt repayment — If the business has bank debt secured by the assets being sold, it has to be repaid at closing. In a share sale, the debt stays inside the company, but it affects the price the buyer is willing to pay.

- Vendor take-back — In many SME transactions, part of the price is paid over several years as a vendor take-back. That amount isn't paid out to you right away — it's a credit the buyer pays down progressively.

The importance of running this calculation before you decide can't be overstated. An owner who negotiates a price without knowing their net amount risks accepting a structure that works against them, or finding out too late that the proceeds don't fund their retirement the way they'd planned.

If you don't yet have a realistic sense of what your business is worth, the first step is still a credible business valuation: the net after tax depends as much on the structure as on a solid starting price. Jean-Luc Rousseau, broker at RCA, walks through the full exercise with concrete numbers in an article that breaks down what's actually left after the sale of a Quebec SME, step by step.

When and how to bring in a tax specialist

If only one idea stays with you from this guide, it should be this: bring in your tax specialist as early as possible. Not when the offer is on the table. Not when the letter of intent is signed. As soon as the sale of your business moves from vague thinking to concrete possibility — even if the horizon is two or three years out.

WHAT A TAX SPECIALIST DOES IN A BUSINESS SALE

Their role goes well beyond the annual tax return. In the context of a sale, the tax specialist:

- Analyzes the optimal structure — share sale vs asset sale, allocation of the purchase price, use of a holding company.

- Plans the LCGE — eligibility review, corporate purification if needed, estate freeze.

- Projects the net amount — estimated tax across different price and structure scenarios.

- Coordinates with the other professionals — the broker, the lawyer, and sometimes the financial planner, so the structure chosen lines up with your retirement goals.

HOW IT WORKS WITH THE BROKER

The broker and the tax specialist play complementary roles, not interchangeable ones. The broker runs the sale process — business valuation, going to market, buyer outreach, negotiating terms, guiding you through to closing. The tax specialist optimizes the structure so the result of that sale is as favorable as possible on the tax side.

In a well-run engagement, the broker consults the seller's tax specialist before finalizing the structure of the transaction. Decisions on price, allocation across asset categories, and vendor take-back conditions all have tax implications the tax specialist has to validate.

We never substitute for the seller's tax specialist. Our job is to structure a transaction that maximizes value. The tax specialist's job is to make sure the seller keeps as much of that value as possible after tax. The two of us have to be talking from day one.

This guide is not professional tax advice

RCA Courtiers is a business brokerage firm. We're not tax specialists, accountants, or legal advisors. The information in this guide is educational and general — it isn't tax advice. Every situation is different. For any decision tied to the tax treatment of your sale, consult a tax specialist experienced in business transactions.