When a buyer receives a valuation built on a single method, they know exactly what to do. They use the other two to negotiate the price down.

That’s why a serious valuation always uses several methods together.

In business valuation, there are three broad families of methods. None of them is perfect on its own. But together, they sketch something much stronger: a defensible value.

Why there isn’t ONE right method

Each valuation method asks a different question:

- Earnings approach: what will the business generate in the future?

- Market approach: how much have similar businesses sold for?

- Asset approach: what are the company’s assets worth today?

These three questions have no reason to land on the same number. And that’s exactly what makes comparing them useful.

If the three methods converge toward the same zone, the price is defensible — in front of a buyer, a lender, and a tax advisor. If they diverge sharply, that’s a signal: there’s something to understand before setting a price.

It’s this cross-checking logic that separates a serious business valuation for Quebec SMEs from a simple rule of thumb.

Earnings approach: DCF and capitalization

The earnings approach looks forward. Its question: how much will the business generate over the coming years, and what is that stream worth today?

Two common variants

Capitalization of earnings is the most direct. You take the normalized EBITDA — the company’s real operating profit — and divide it by a rate that reflects the risk and size of the business.

The capitalization rate — 25% here — factors in several things: the size of the business, how diversified its customer base is, owner dependency, revenue recurrence, and industry risk. The higher the perceived risk, the higher the rate — and the lower the value.

DCF (Discounted Cash Flow) is more detailed. You project cash flows over 5 to 7 years, estimate what the business will be worth beyond that horizon (the terminal value), then bring the whole thing back to today’s value — because a dollar five years from now is worth less than a dollar today.

DCF is more sensitive to assumptions — but it’s also the only method that explicitly captures future growth.

Simplified example

Picture a Quebec manufacturing SME with a normalized EBITDA of $1,200,000.

Applying a 25% capitalization rate:

$1,200,000 ÷ 25% = $4,800,000

That number isn’t a price. It’s an order of magnitude the earnings approach suggests, in this specific example, with these specific assumptions.

Strengths and limits

- Strength: it’s the only approach that looks ahead. It captures growth potential and revenue recurrence.

- Limit: it’s sensitive to assumptions. Move the capitalization rate by a few points and the value swings by hundreds of thousands of dollars.

When we build a DCF at RCA, the first thing we stress-test is the robustness of the assumptions — not the final number. A model that produces a reassuring figure on the back of a fragile assumption doesn’t protect the seller in negotiation.

Market approach: comparable transactions

The market approach looks sideways. Its question: how much have comparable businesses actually sold for?

How it works

You identify recent transactions in the same sector, for businesses of similar size. You extract the EBITDA multiple paid in each transaction. Then you apply that multiple to the normalized EBITDA of the business being valued.

Sources vary — specialized databases, broker networks, public data for the largest transactions.

In practice, finding good comparables for an SME takes work. Private transactions aren’t disclosed the way public-company deals are.

A broker active in the Quebec market builds up a working knowledge of recent transactions that complements the formal databases. That’s a real edge: the more reference points the broker has, the sharper the comparable.

Example

Take the same SME.

If similar manufacturing businesses have recently sold around 3.5x EBITDA — a multiple common in this type of sector — you get:

$1,200,000 × 3.5 = $4,200,000

That’s a different anchor point from the DCF. Lower in this case — which is common, because the real market is often more conservative than theoretical projections.

Strengths and limits

- Strength: grounded in reality. It’s often the most convincing argument in front of a buyer, because these are real transactions.

- Limit: every business is unique. A comparable is never a perfect match. And private-SME data isn’t always accessible.

What comparables show is the range the market is willing to transact in. Not a precise figure — a zone.

Asset approach

The asset approach looks underneath. Its question: what are the company’s tangible assets worth, once liabilities are subtracted?

How it works

You take the assets on the balance sheet — equipment, inventory, accounts receivable, real estate if there is any — adjust them to their fair market value, and subtract the liabilities.

The result is the adjusted net asset value.

Example

For our manufacturing SME, let’s say the adjusted net asset value works out to around $3,200,000.

That figure reflects the value of physical and financial assets. It doesn’t capture customer relationships, reputation, the team’s know-how, or revenue recurrence — what we call goodwill.

When it’s relevant

The asset approach is especially useful for:

- asset-heavy businesses (manufacturing, transport, real estate)

- liquidation or forced-sale situations

- files where goodwill is small relative to tangible assets

For a services business with few physical assets, this method often produces a very low figure — which doesn’t mean the business is worth nothing. It means its value lies elsewhere: in its contracts, its customers, and its earnings power.

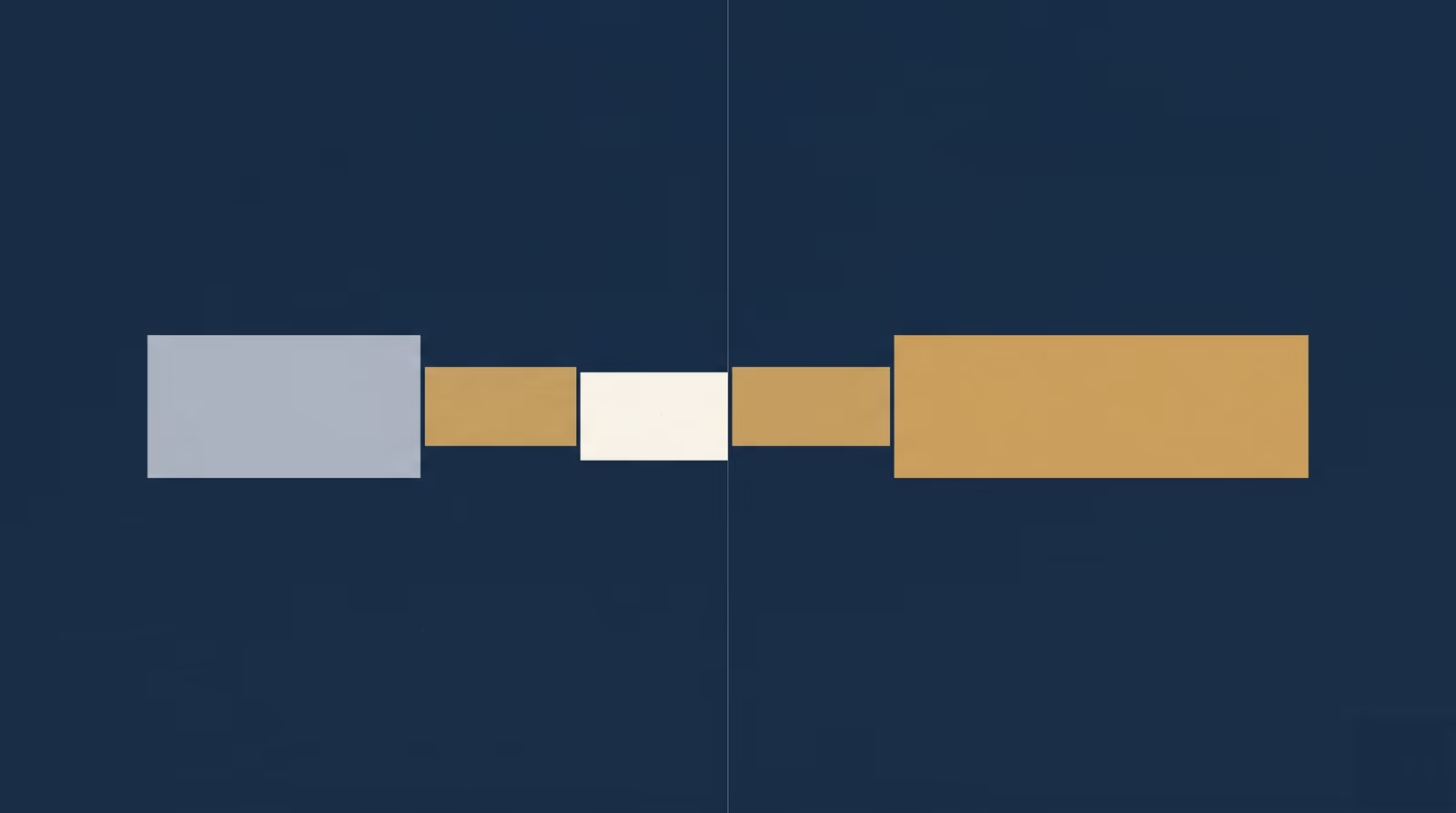

The three methods side by side

Here’s what the three approaches produce when applied to the same SME:

| Method | Question | Result | Best for | Limit |

|---|---|---|---|---|

| Earnings (DCF / capitalization) | What will the business generate? | ~$4.8M | Growth, recurring revenue | Sensitive to assumptions |

| Market (comparables) | How much have similar ones sold for? | ~$4.2M | SMEs with accessible comparables | Limited private data |

| Assets (adjusted net asset value) | What are the tangible assets worth? | ~$3.2M | Asset-heavy, manufacturing | Doesn’t capture goodwill |

Three methods, three results: $3.2M, $4.2M, and $4.8M.

The defensible value does not mechanically come from averaging the three. It is built inside that discussion range, based on the company’s profile, the sector, the quality of the results, and what a realistic buyer can finance.

How a broker uses these methods

A strictly accounting-based view can sometimes emphasize one dominant method — for example net asset value or capitalization. That isn’t a mistake. But it is not always enough to defend a price in the market.

A broker uses the three approaches together because each one lights up an angle the others don’t see.

When the results converge, we know the price rests on a solid base. When they diverge, that’s a signal: we need to understand why before taking the file to market.

At RCA, we use all three approaches together — earnings, market, assets. Not to complicate the process. So that the price we defend holds up in front of a buyer, a lender, and a tax advisor.

The difference isn’t theoretical. A seller who walks into negotiation with a single-method valuation often ends up defending a number the buyer can easily push back on. A seller who walks in with a valuation supported by three angles changes the dynamic.

The goal is not to choose the method that gives the highest number. It is to understand which price can be defended, explained, and supported in front of the people who need to accept the transaction.

Key takeaways:

- Three families of methods, three angles — earnings (future), market (reality), assets (floor)

- No method stands alone — using them together is what produces a defensible value

- Convergence between methods reinforces the price — divergence is a signal to investigate

- A broker cross-checks these approaches to defend the price — not to produce an isolated accounting view