The bank finances the buyer. The buyer puts up their down payment. And there’s still a gap.

That gap is often filled by the seller — through a vendor take-back.

What a vendor take-back is

A vendor take-back — or VTB — is a portion of the price the seller agrees to receive after closing, over a defined period.

In practice: instead of cashing the full price on signing day, the seller “lends” part of the amount to the buyer. That amount is repaid over 2 to 5 years, with interest.

It’s a common financing mechanism in Quebec SME transactions. It isn’t a sign that the deal is weak — it’s a normal piece of the financing structure.

The VTB shows up in the letter of intent (LOI) as one of the components of the price. That’s when it’s negotiated — not later. A well-structured LOI can shift several hundred thousand dollars in the seller’s favour.

Understanding how it works is part of the foundation of the process of selling a business in Quebec.

Why it’s so common

In an SME sale, the financing is rarely simple.

The bank will lend part of the acquisition price — but rarely all of it. The buyer puts up a down payment — but it’s often not enough to cover the rest.

The VTB closes the gap between what the bank lends and what the buyer can put up out of pocket.

From the lender’s point of view, a VTB can be a positive signal, if it’s properly structured. If the seller agrees to finance part of the price, it means they believe in the business — and in the buyer’s ability to run it. That can lower the risk the bank perceives.

The more comfortable the lender is with the structure, the more likely the financing is to hold. In other words: a VTB can help the seller defend a better total price — even if they don’t receive everything on day one.

That’s also why strategic buyers — those with synergies or more capital — often ask for a smaller VTB, or none at all. They have the means to close the financing structure another way.

What’s normal

In SME transactions, the VTB often falls between 10-30% of the sale price — depending on the file, the financing structure, and the buyer’s profile. That’s an order of magnitude, not a fixed rule.

What moves the number:

- The size of the transaction: the bigger it is, the more financing sources are available — and the smaller the VTB weighs in proportion.

- The buyer’s strength: a buyer with a substantial down payment and a strong financial profile will need less VTB.

- The quality of the file: a business with a stable EBITDA, diversified customers, and few risks attracts better bank financing — so less VTB.

- The lender’s appetite: depending on market conditions and the sector, banks finance more or less generously.

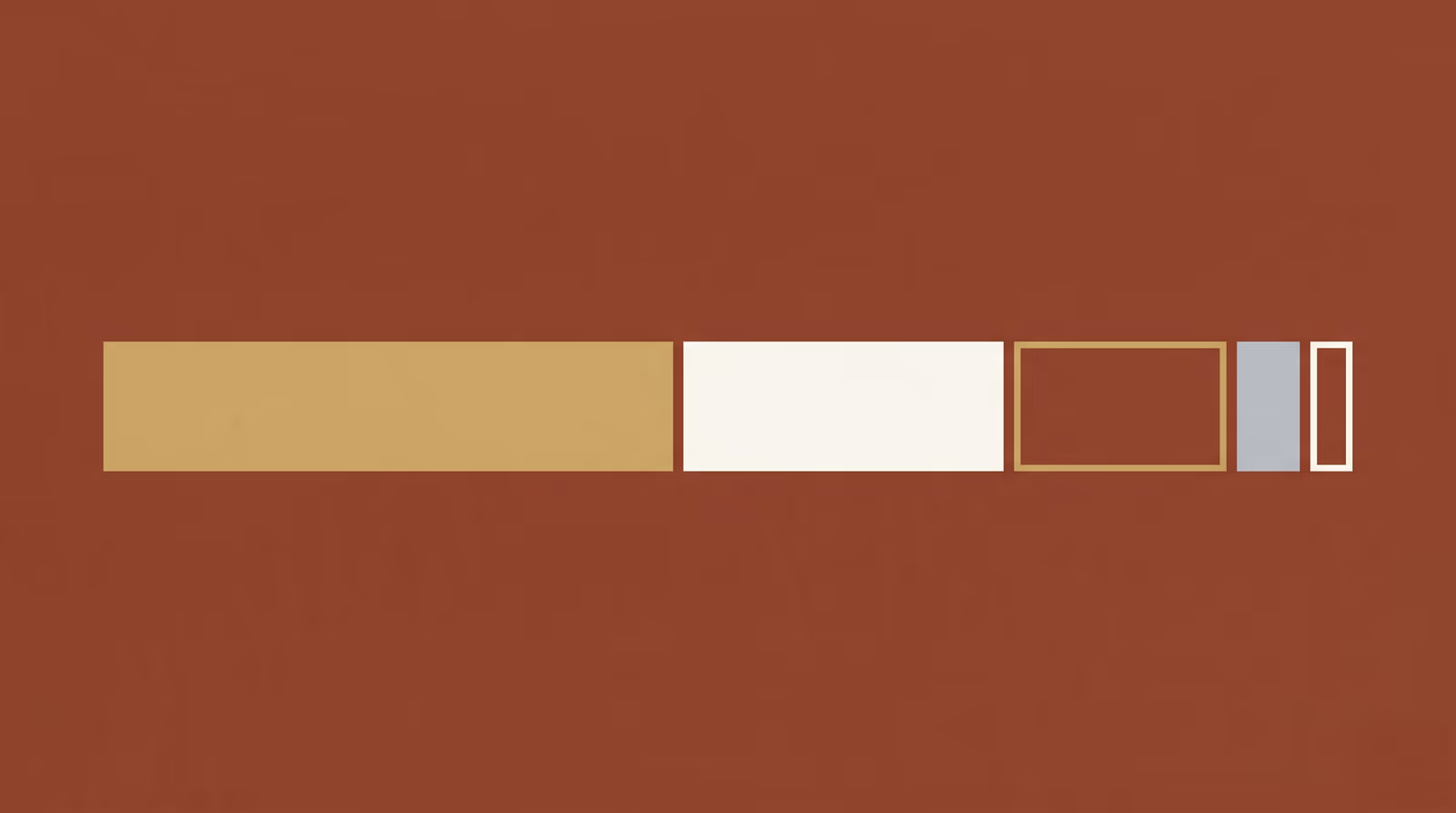

Sample structure

Take a simplified $3 million transaction:

| Component | Amount | % of price |

|---|---|---|

| Buyer’s down payment | $500,000 | 17% |

| Bank financing | $2,000,000 | 67% |

| Vendor take-back (VTB) | $500,000 | 17% |

| Total price | $3,000,000 | 100% |

In this example, the VTB is the piece that closes the structure. Without it, the buyer would need to find another $500,000 in down payment — which is rarely possible. Or the bank would have to lend more, which it may refuse if the risk becomes too concentrated.

How to protect yourself as a seller

A VTB should never be a handshake. It’s a loan — and like any loan, it has to be structured with clear, documented terms.

Here are the five elements to negotiate:

1. Duration

Typically 2 to 5 years. The shorter the duration, the faster the seller gets their money back. But a duration that’s too tight can put the buyer in a cash flow strain — which is in nobody’s interest.

2. Interest rate

The VTB carries interest — at the market rate or slightly above. The seller is taking a risk by financing the buyer. The rate has to reflect that risk.

3. Collateral

Security on the business’s assets — equipment, accounts receivable, inventory — can protect the seller in the event of default, depending on the rank accepted by the senior lender. Without collateral, the VTB is an unsecured loan — and the seller carries much more risk.

4. Repayment terms

Monthly or quarterly payments? Fixed amount or balloon at maturity? Option for early repayment?

The terms have to be clear and documented in the purchase and sale agreement.

5. Subordination

The VTB is almost always subordinated to the bank loan — meaning the bank gets paid back first.

That’s the norm. But the seller has to understand what it means in practice: if the business runs into financial trouble, the lender comes ahead of the seller in line for repayment. Even with collateral, the seller may therefore sit behind the bank in the repayment order.

When to refuse or push back

A VTB isn’t mandatory. It’s a negotiation tool — not an automatic condition of every transaction.

The tax implications of a business sale also shift depending on the structure: a VTB may sometimes allow the seller to defer tax on part of the capital gain to the years when payments are received. This point should be validated with the tax advisor.

Here are the situations where it’s reasonable to refuse or renegotiate:

The VTB is too high. When the VTB approaches or exceeds 40% of the price, the question comes up: does the buyer have enough money truly at risk? If most of the risk rests on the seller and the bank, the buyer has little to lose if things go wrong — and that isn’t a healthy balance.

The collateral is insufficient. A VTB without security is a leap of faith. The seller deserves more than a verbal promise for an amount in the hundreds of thousands of dollars.

The buyer can’t demonstrate their capacity. If the buyer doesn’t have the experience, the business plan, or the resources to run the business and repay the VTB, the seller is carrying a disproportionate risk.

In all these cases, the right reflex isn’t necessarily to walk away from the transaction. It’s to renegotiate the terms — or to find a better-financed buyer.

Before negotiating a vendor take-back, you first need to understand which financing structures are realistic for your business. A confidential valuation can be a useful starting point.

Key takeaways:

- VTBs are normal in SME deals — they close the gap between the bank and the buyer's down payment

- Often between 10-30% of the price — depending on the file, the structure, and the buyer's profile

- Five terms to negotiate — duration, rate, collateral, repayment, subordination

- A VTB isn't mandatory — near 40% or more, question the balance of the structure