Two manufacturing businesses. Same industry, same revenue, same EBITDA. One sells at 3.5x. The other at 5x.

The difference isn’t a mystery. It comes from the quality of the business, the risk buyers perceive and the buyer pool the file can attract.

A valuation multiple isn’t a fixed number you apply automatically. It’s a result — the result of profitability, growth and the specific risk tied to your business.

What a valuation multiple is

The valuation multiple is the most direct way to estimate what a business is worth.

The formula:

Enterprise value = normalized EBITDA × multiple

Normalized EBITDA is the real operating profit of the business — once owner-specific items and non-recurring expenses are stripped out. The multiple is the factor a buyer is willing to pay for every dollar of EBITDA.

In practice:

- Normalized EBITDA of $2,000,000 × 4x = value of $8,000,000

- The same EBITDA × 5x = $10,000,000

A single point of multiple up or down, on a $2,000,000 EBITDA, is $2,000,000 in value. That’s why understanding what drives your multiple is one of the most important questions in business valuation.

Important: enterprise value is not the net amount that ends up in your pocket. To make that bridge, separate enterprise value from what is actually left after the sale.

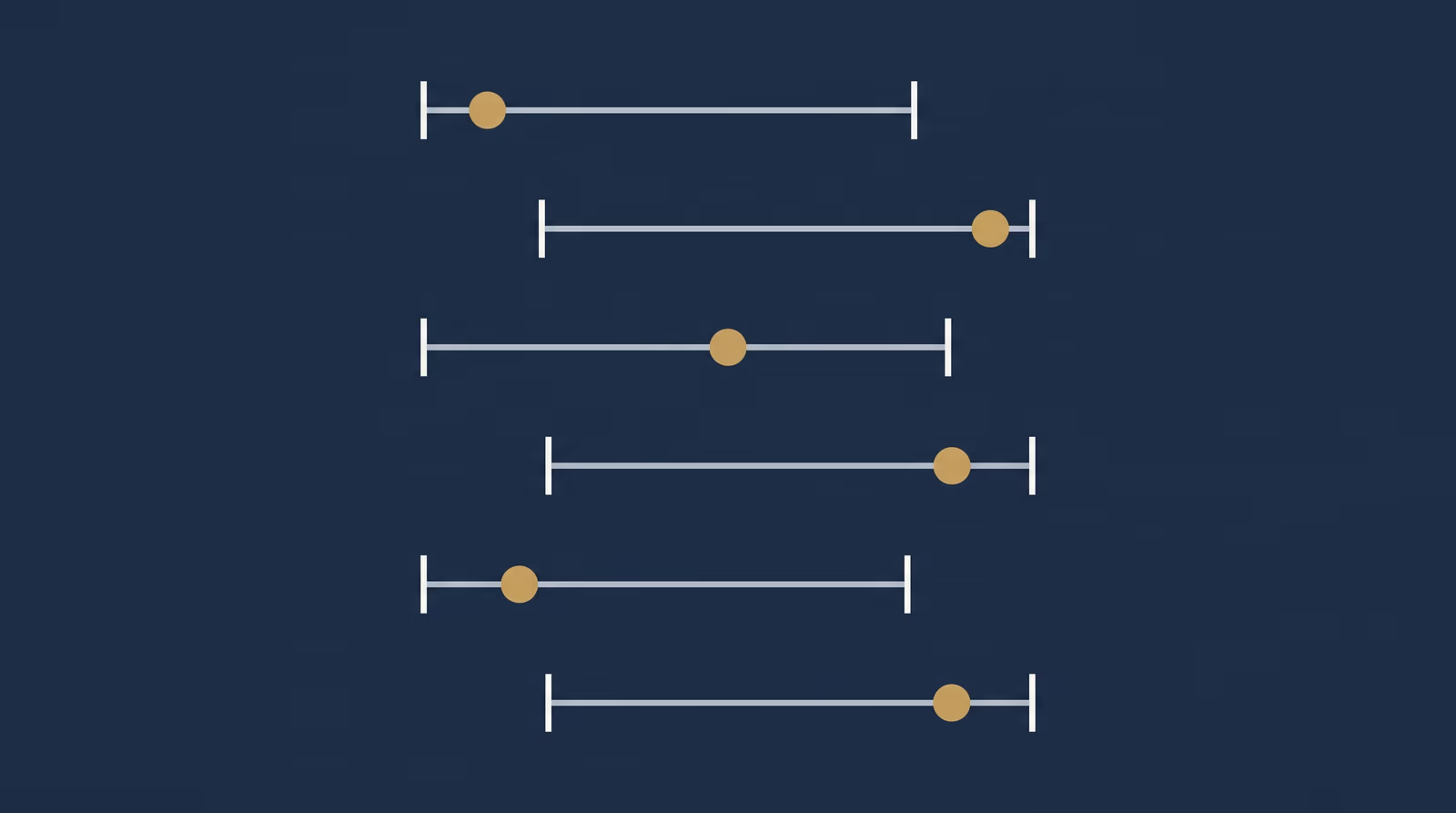

Multiples by industry — indicative ranges

The ranges below are indicative. They are meant mainly for Quebec SMEs generating roughly $3 million or more in revenue, in transactions where buyers are looking at normalized EBITDA.

Each range groups several sub-segments. A dealership is not valued like a collision repair shop. A technology firm with recurring revenue is not valued like a custom development team.

For the breakdown by profile, see the linked industry page.

| Industry | Range | What pushes it higher |

|---|---|---|

| Manufacturing | 2.5x – 8x | Proprietary product / IP, certifications, modern equipment |

| Technology | 3x – 10x | Recurring contracts, mature cybersecurity |

| Distribution | 3.5x – 8.5x | Platform > $5M EBITDA, value-added services, stable margins |

| Professional services | 4x – 12x | Recurring mandates, engineering backlog, team autonomy |

| Construction | 3x – 8x | Recurring services, diversified backlog, autonomous team |

| Healthcare | 5x – 8.5x | EBITDA > $1M, consolidator appetite |

| Agri-food | 4x – 8x | Own brand, GFSI certifications, customer diversification |

| Transportation / Logistics | 3.5x – 9x | Asset-light model (3PL), long-term contracts, recurrence |

| Automotive | 2.5x – 6.5x | Autonomous team, low insurer concentration, certifications |

Two things to note.

First, the ranges are wide. That’s normal. Two businesses in the same industry with the same EBITDA can end up at opposite ends of the range.

Second, these numbers don’t apply to very large transactions or to the U.S. market. Quebec SMEs trade in a specific market, with its own buyers, its own financing conditions and its own realities.

What moves the multiple

The industry gives you a range. Your company’s profile decides where you sit inside that range.

Here are the five factors that matter most.

1. Company size

All else equal, a larger business usually earns a higher multiple.

A $1.5M EBITDA attracts more buyers — often better-financed ones — than a $300,000 EBITDA. The wider the buyer pool, the more competitive pressure pushes the price.

It isn’t a question of intrinsic quality. A smaller company can be run perfectly well — but its pool of potential buyers is narrower.

2. Revenue growth

A business growing steadily at 10 to 15% a year sits in the upper part of its range. A business with flat or declining revenue lands in the lower part — regardless of industry.

A buyer buys the future, not just the present. A track record of sustained growth is the most direct signal that the future is promising.

3. Revenue recurrence

Long-term contracts, subscriptions, recurring service agreements — all of it reduces the risk a buyer perceives.

That’s the main reason SaaS tech businesses earn such high multiples. Their revenue is predictable, measurable and recurring.

On the other hand, a business that starts from zero every year — no backlog, no contracts — carries a risk the multiple reflects.

4. Customer concentration

If a single customer represents 30% or more of revenue, the multiple drops. Losing that customer means losing a disproportionate share of the value.

A buyer and their lender will quantify that risk — and fold it straight into the price they’re willing to pay.

5. Owner dependency

If the business can’t run without the owner, that’s a problem for the buyer.

A buyer is buying a business, not a job. That’s why owner dependency is the factor that most often weighs on the multiple in Quebec SME files. The more autonomous the team in place — management, sales, operations — the better the multiple holds.

A business where the owner is everywhere is a business the buyer will have to rebuild after the sale. And that shows up in the price.

To go deeper on these factors, see the article on the factors that drive business value.

The pitfalls of “average” multiples

“My accountant told me it’s 5x in my industry.”

Maybe. But an average multiple says almost nothing about your specific business.

The average includes the best companies in the industry — the ones with strong growth, recurring revenue and a solid team. It also includes the weakest ones — the ones with a dominant customer, an irreplaceable owner and a declining EBITDA.

Your business isn’t the average.

The trap runs two ways:

- For the seller: a multiple set too high creates an expectation the market won’t validate. Worse, it can scare off serious buyers before the conversation even starts.

- In negotiation: a buyer who sees a seller anchored to a multiple with no justification knows exactly how to take it apart.

On the buyer’s side — and with the lenders who finance most Quebec SME transactions — the question is never “does this business deserve a 5x?”. The question is “do the numbers support a 5x — and will the bank go along?”.

A defensible multiple isn’t a number you quote. It’s a number you can explain — with the company’s data, market comparables and a financial model that backs it up.

How to use these numbers

The ranges in this article are a starting point, not a conclusion.

Use them to:

- calibrate your expectations before entering a process

- understand where your industry sits relative to others

- identify the factors to work on to improve your position in the range

But to get the real multiple for your business, you have to combine this data with a DCF, specific comparable transactions and a full analysis of your file.

That’s the difference between an industry range and a valuation. And it’s also the number everything else builds from — preparing the file, qualifying buyers, the concrete steps to sell a business in Quebec.

At that point, the right reflex is not to pick the multiple you prefer. It is to build the file that lets a buyer see it.

Key takeaways:

- A multiple is a result, not an entitlement — it depends on the specific profile of your business

- Industry ranges run from 2.5x to 12x — but your position inside the range depends on five key factors

- An "average" multiple is misleading — your business isn't the average of its industry

- A defensible multiple has to be justified — with data, comparables and a model, not with a hunch